")

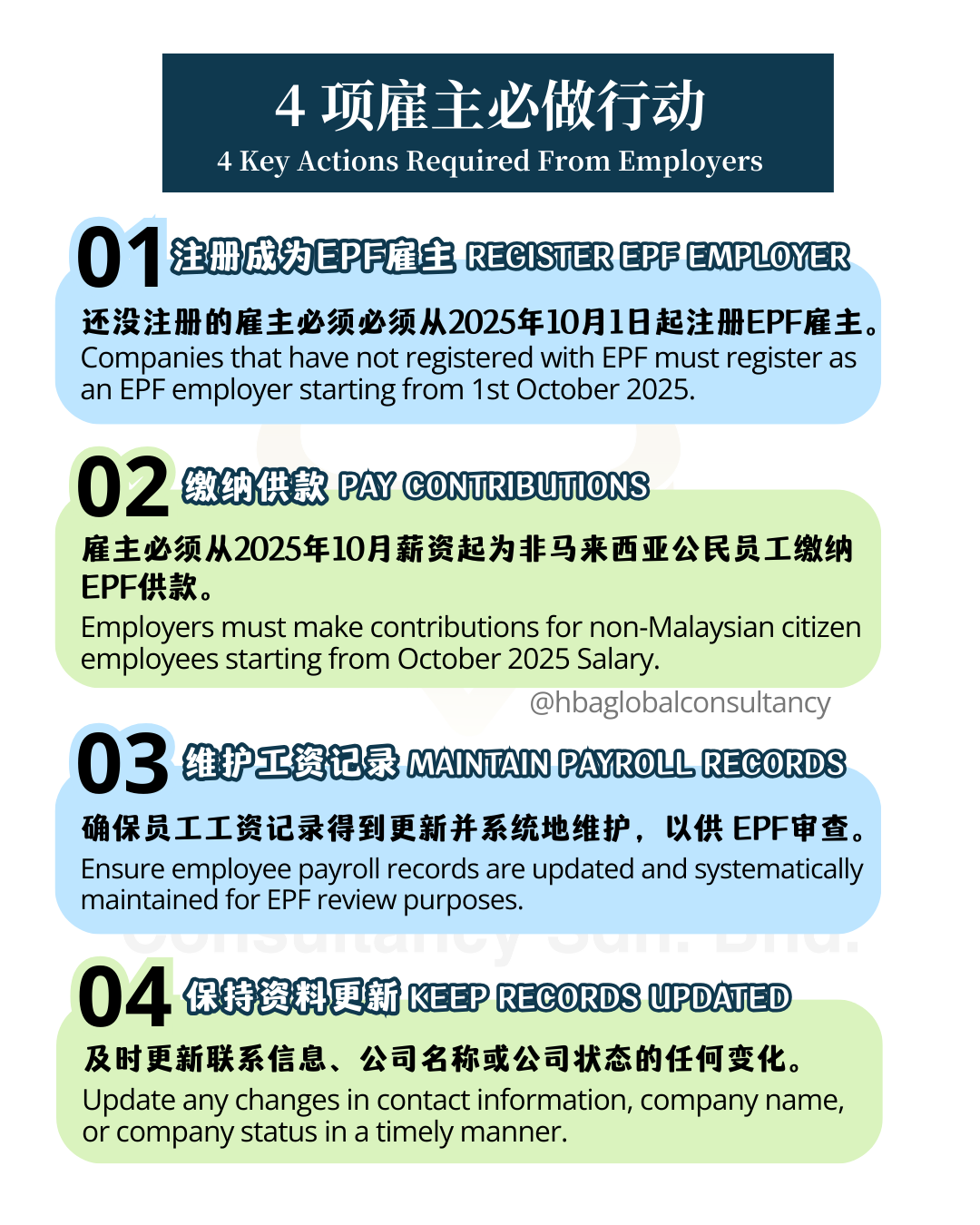

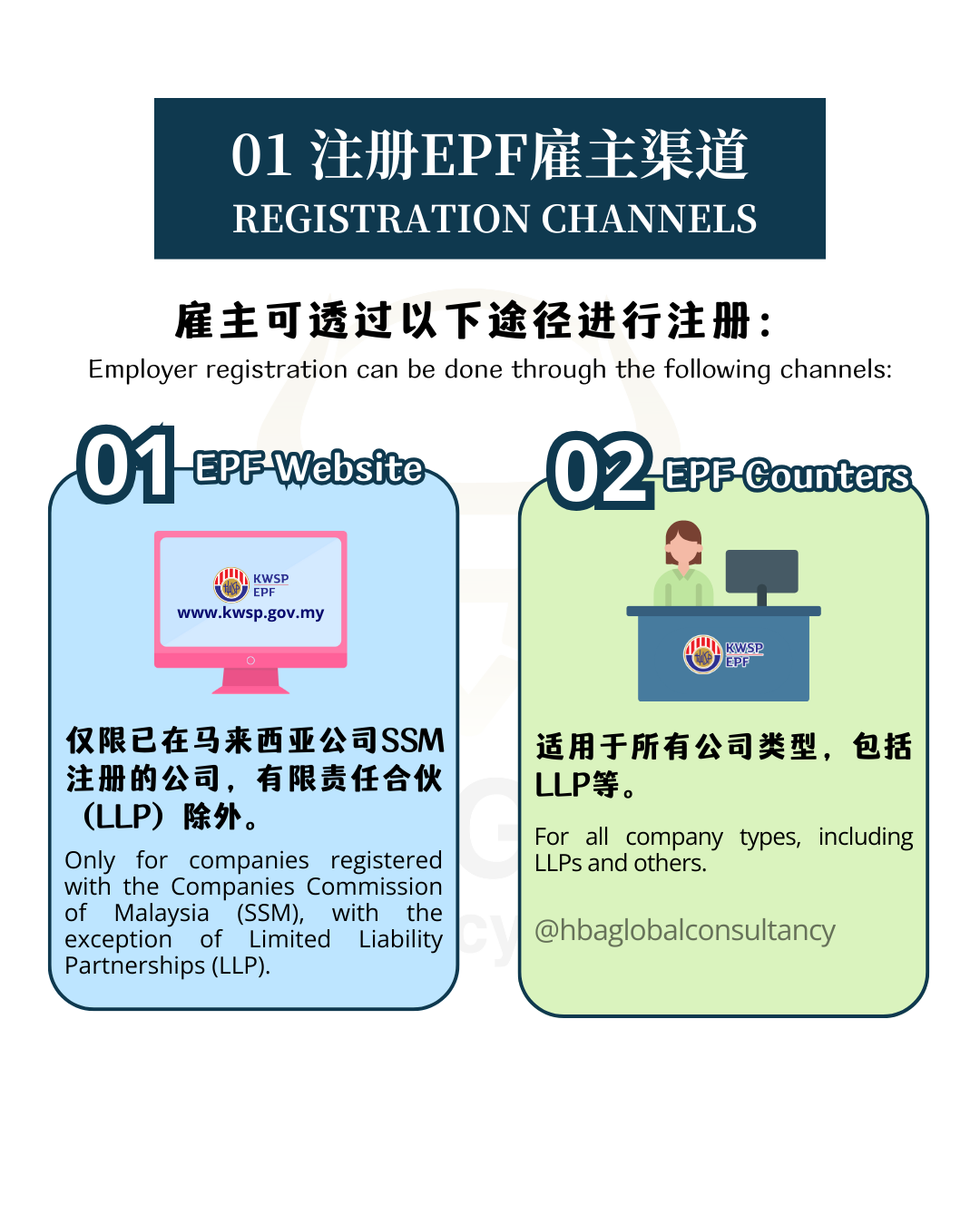

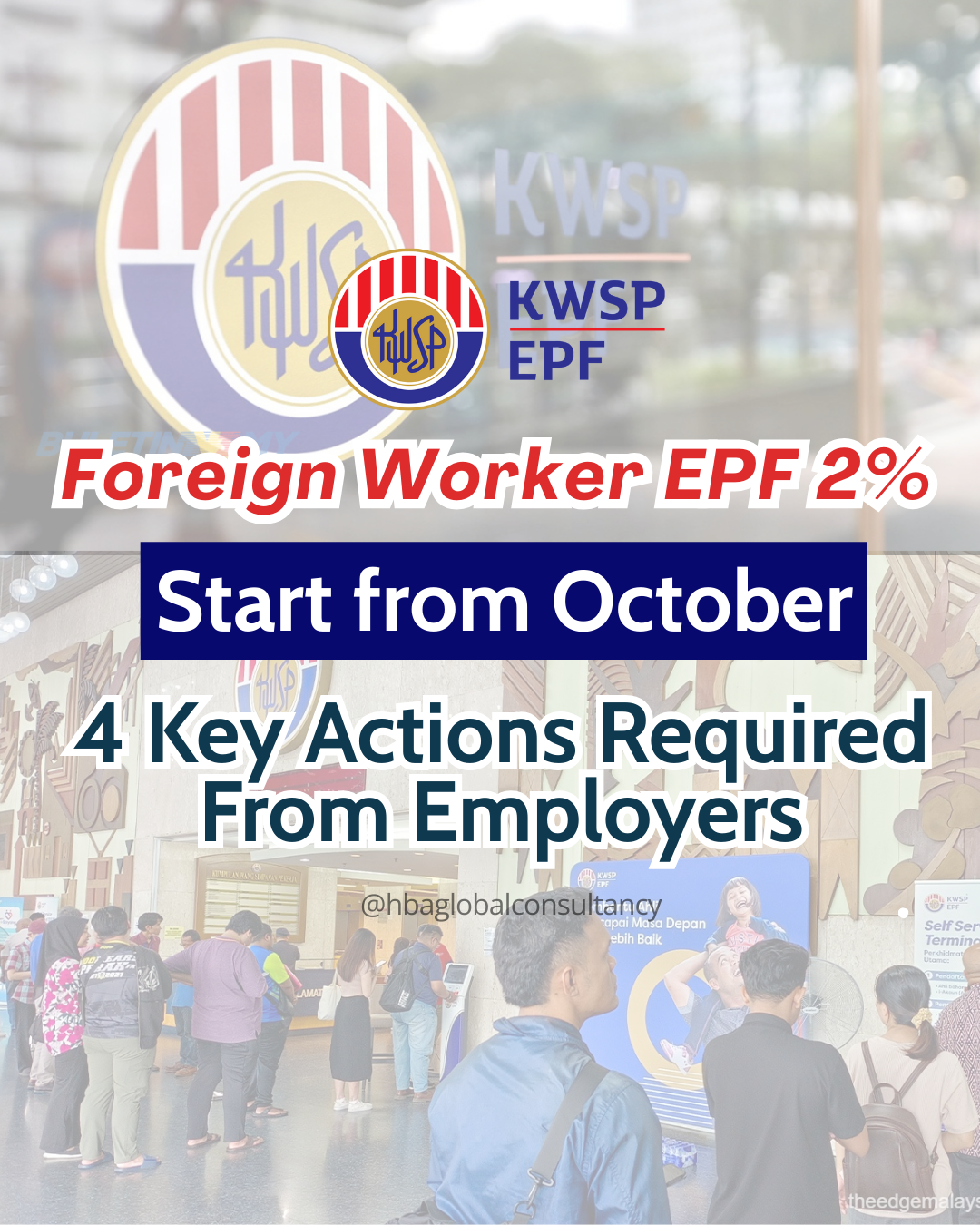

尚未注册EPF的公司必须从2025年10月1日起注册成为EPF雇主。

已有活跃EPF雇主账户的公司可继续使用现有账户,无需重新注册。

EPF网站(仅限已在SSM注册的公司,LLP除外)

EPF柜台(适用于所有公司类型,包括LLP)

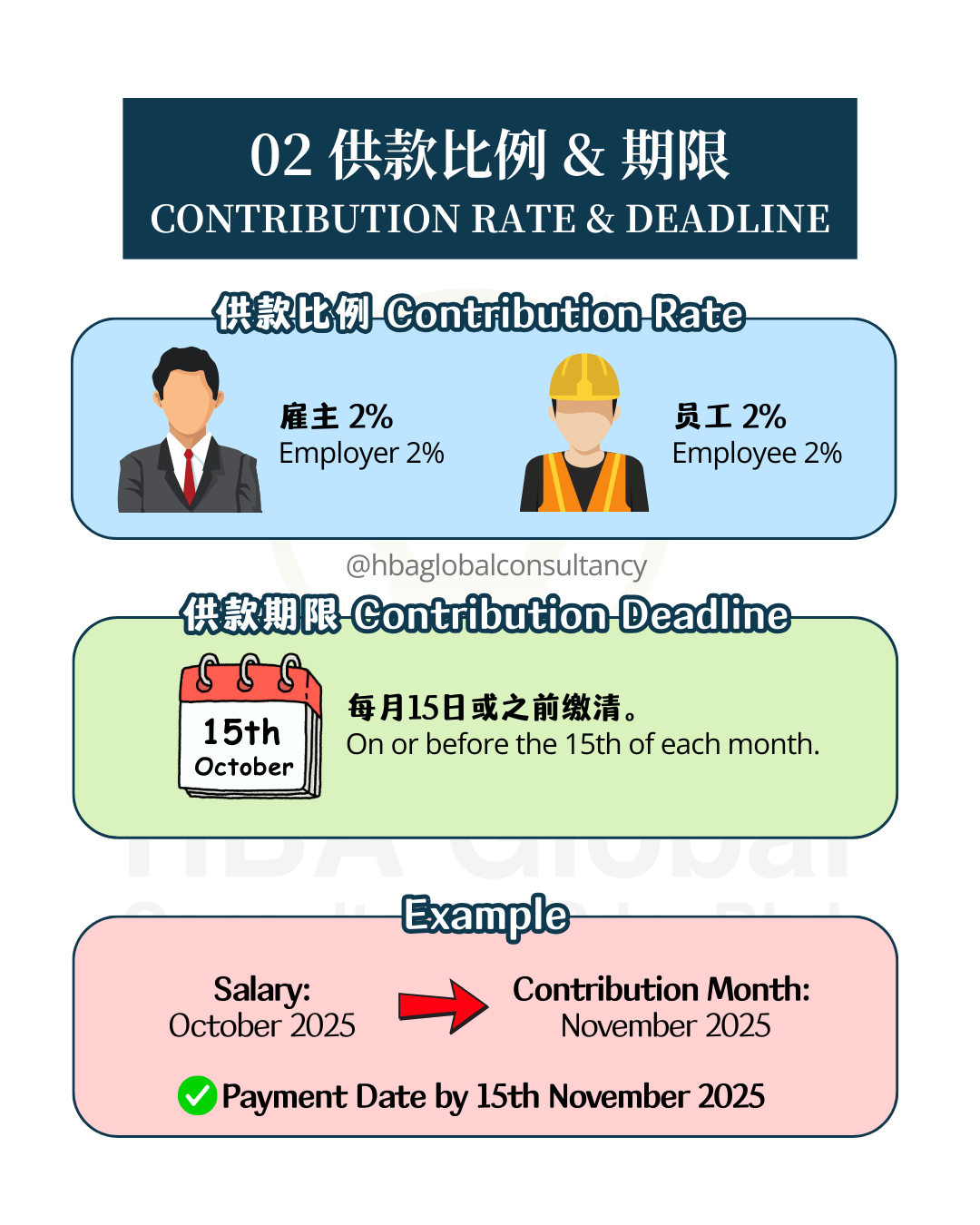

雇主必须从2025年10月薪资起为非马来西亚公民员工扣缴并缴纳供款。

供款比例:雇主 2%,员工 2%。

供款期限:必须在隔月15号或之前缴清。

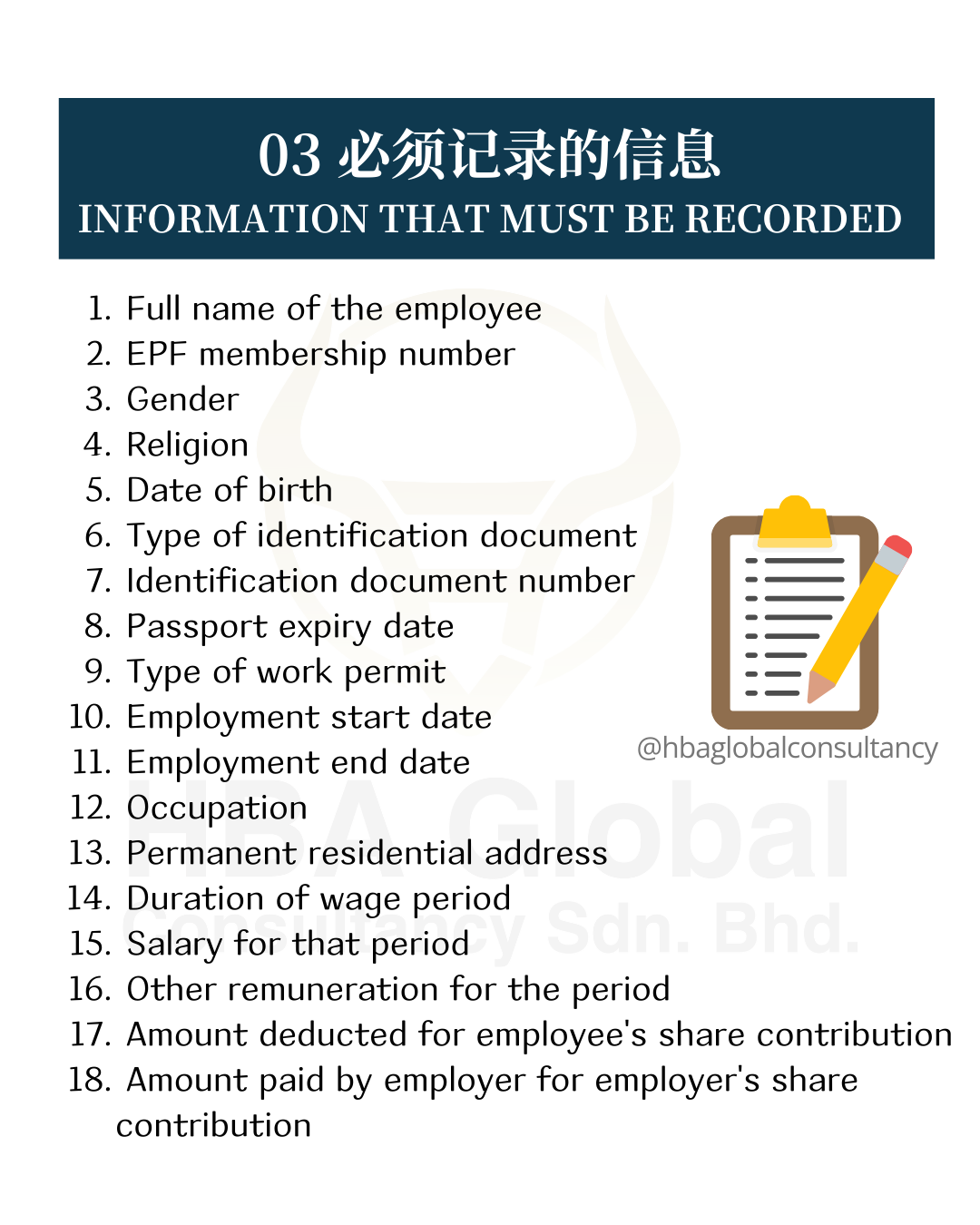

需记录以下员工信息,以备EPF审核:

员工全名

EPF会员编号

性别、宗教、出生日期

证件类型及号码

护照到期日

工作准证类型

入职及离职日期

职位

常住地址

工资支付周期及薪资

其他报酬

员工供款额(扣除部分)

雇主供款额

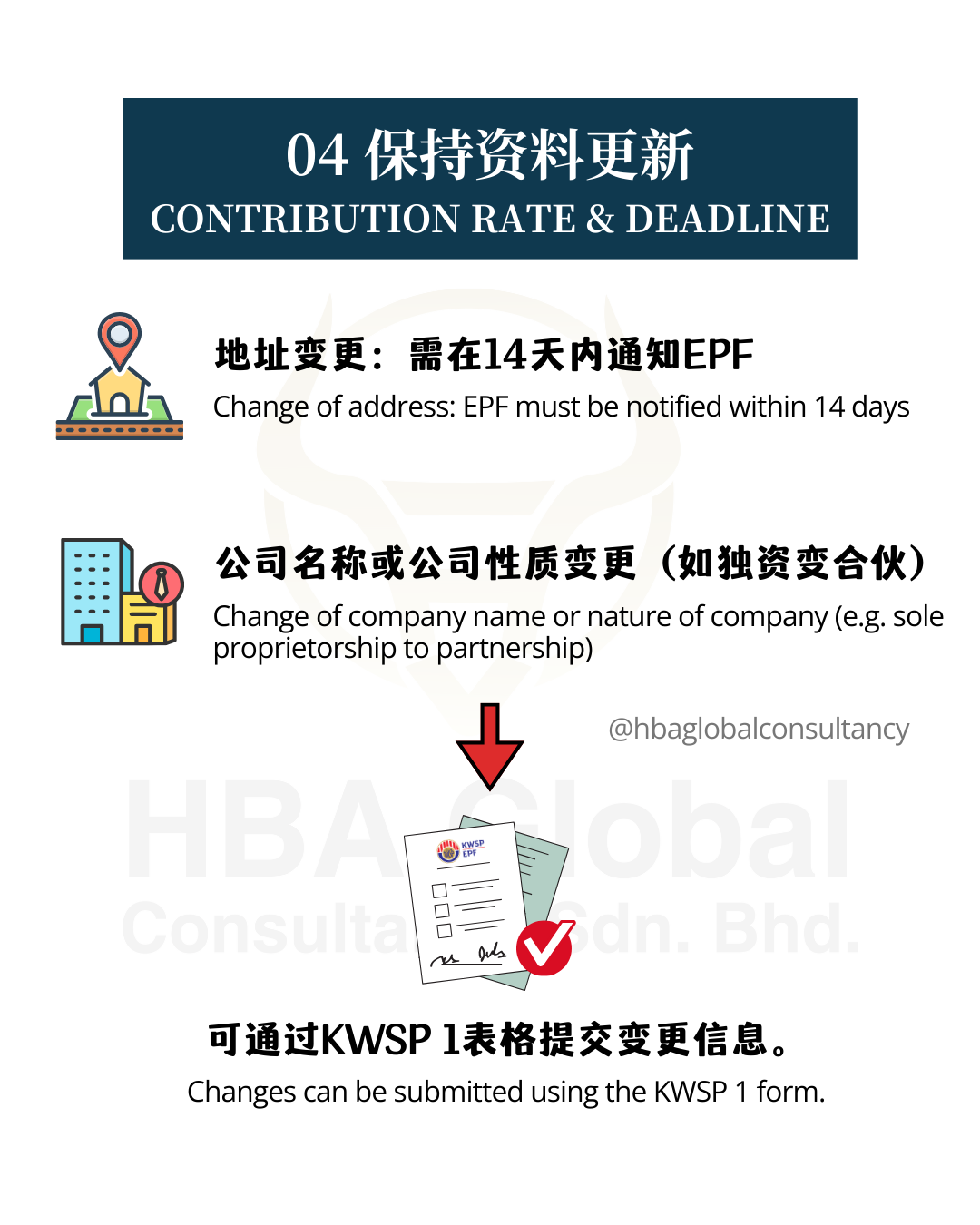

地址变更:需在14天内通知EPF。

公司名称或公司性质变更(如独资变合伙):需在21天内通知EPF。

使用KWSP 1表格提交变更信息。

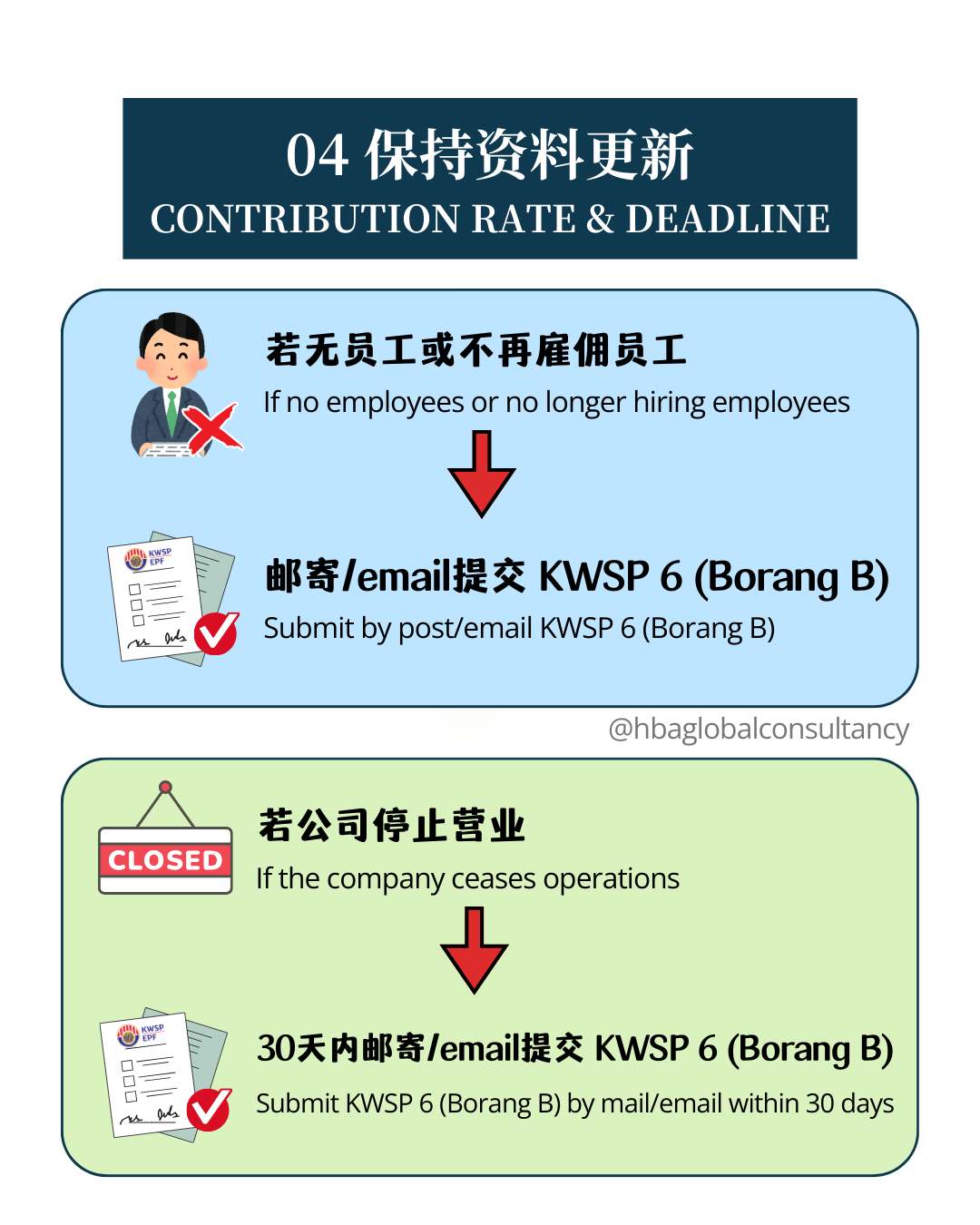

若不再聘请员工或停止营业,必须在30天内通过邮寄/电邮提交KWSP 6(表格B)。

Companies that have not registered with EPF must register as an EPF employer starting from 1st October 2025.

Employers with an active EPF employer account may continue using their existing account and are not required to register again.

EPF Website (Only for SSM-registered companies, excluding LLPs)

EPF Counters (All company types, including LLPs)

Employers must deduct and remit contributions for non-Malaysian citizen employees starting with the October 2025 salary.

Contribution Rate: 2% employer’s share, 2% employee’s share.

Contributions must be paid on or before the 15th of the following month.

需记录以下员工信息,以备EPF审核:

Full Name

EPF Membership No.

Gender, Religion, Date of Birth

ID Type & Number

Passport Expiry Date

Work Permit Type

Employment Start & End Date

Occupation

Permanent Address

Wage Period, Salary & Other Remuneration

Contribution Deductions (Employee & Employer Share)

Inform EPF of any address change within 14 days.

Inform EPF of company name or status changes (e.g., Sole Proprietorship → Partnership) within 21 days.

Notify EPF using Form KWSP 1.

If the company no longer has employees or has ceased operations, notify EPF within 30 days via KWSP 6 (Form B) (mail/email/other channels).

")

如何在 MyTax 搜索 Tin Number?

TIN Number是实施电子发票时需要的资料,许多老板在这期间头痛供应商/顾客不提供TIN Number, 税务局已经听到我们的心声!

现在可以到MyTax官网搜索对方的Tin Number,只需拿到:

✅ IC Number

✅ Passport Number

✅ SSM Registration Number

就能快速查找Tin Number!

⚠️ 温馨提醒:

请勿滥用此功能,否则可能面临:

🚫 高达RM4,000罚款

🚫 长达1年监禁

您可以通过以下步骤快速找到TIN号码:

登录 MyTax:https://mytax.hasil.gov.my/ 并点击“Carian TIN”

对于个人/Enterprise,选择:

对于其他,请选择:

输入公司注册号码,您将获得TIN:

The TIN Number is required when implementing e-Invoicing. Many business owners have been frustrated during this period because suppliers/customers refused to provide their TIN Numbers, but the tax authority has heard our concerns! 😂

You can now search for the other party’s TIN Number on the MyTax official website. All you need is:

✅ IC Number

✅ Passport Number

✅ SSM Registration Number

⚠️ Friendly reminder:

Do not misuse this function, or you may face:

🚫 A fine of up to RM4,000

🚫 Imprisonment of up to 1 year

You can quickly find the TIN Number with the following step:

For Individual/Enterprise, Choose:

For Others, Choose:

Insert the company registration number, you will get the TIN:

")

2025 Malaysia SST (Sales and Service Tax) Guide for Various Service Industries

")

可以。任何合伙人或债权人皆可在以下日期中较迟的 30天内提出异议:

发出通知给合伙人的日期,或

报章刊登通知的日期

📮 异议必须以书面形式提交至:

Director

Registration Services Division (Insolvency Section)

Suruhanjaya Syarikat Malaysia (SSM)

Level 19, Menara SSM@Sentral

No. 7, Jalan Stesen Sentral 5

Kuala Lumpur Sentral, 50623 Kuala Lumpur

Email: enquiry@ssm.com.my

VW101 - LLP 解散声明通知

VW107 - 分配完成通知(即使 LLP 没有任何资产也必须提交)

须在资产分配完成后的 14天内 提交

解散申请必须在以下日期中较迟的 7天内提交:

合伙人通知日期,或

报章广告日期

VW101 与 VW107 均为线上表格,无需提交纸本副本

指南中提供马来文及英文广告样本(附录A和B),以及法定声明样本供参考

这篇文章参考马来西亚SSM官方网站

Director

Registration Services Division (Insolvency Section)

Suruhanjaya Syarikat Malaysia (SSM)

Level 19, Menara SSM@Sentral

No. 7, Jalan Stesen Sentral 5

Kuala Lumpur Sentral, 50623 Kuala Lumpur

Email: enquiry@ssm.com.my

Let our team assist you from preparation to submission✅

👉 Contact us today for a consultation.

Info are refer from Malaysia Official SSM Website:

")

Preparation by Company Secretary:

Cover letter to SSM

Directors’ declaration

Shareholders’ resolution

Latest management accounts

Relevant supporting documents

Submission:

Application submitted to SSM

Publication:

SSM will publish a Notice in the Gazette

If no objections arise, the company will be officially struck off the register

Reinstatement Risk: SSM may reinstate the company within 7 years if there’s evidence of continued business activity.

Cost-Effective: Generally cheaper than voluntary liquidation.

Director’s Liability: Directors may still be liable for offences committed before dissolution.

Tax Clearance: Required from LHDN (may be waived for dormant companies)

Our experienced team can guide you from assessment to application.

👉 Contact us today for a consultation.